At first glance, buy now, pay later (BNPL) sounds like a win-win: lower upfront costs for shoppers, higher conversion rates for retailers. No interest. No pressure. Just flexibility.

But is BNPL - also known as an installment payment plan - really a gentler form of credit? Or is it simply debt in disguise?

Ivey Business School marketing professor Miranda Goode breaks down how the process really works, why retailers love it and what consumers should be thinking about before clicking "confirm."

First things first: what exactly is ’buy now, pay later,’ and how is it different from putting something on a credit card?

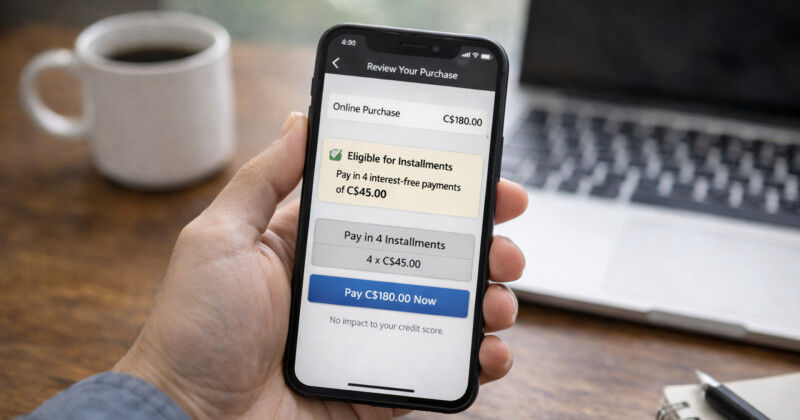

Miranda Goode (MG): "Credit on training wheels," is how Patrick Chan of Sezzle describes BNPL, and I agree. Today, those training wheels are embedded in the online shopping experience, with consumers routinely offered the option to split purchases into smaller, easy payments at checkout through providers such as Affirm, Afterpay, Sezzle, Shop Pay, Klarna and even Canada’s major financial institutions.

While BNPL transactions may still involve a linked credit card or direct access to a bank account, consumer appeal is straightforward: smaller upfront payments make purchases feel significantly more affordable than paying the full amount at once.

BNPL usage has exploded in the last few years. From a business perspective, what’s driving retailers to adopt these options so aggressively?

MG: BNPL options may give retailers access to consumers who would have otherwise not purchased at all’or deferred purchases until a later date. Yes, this sounds dark, because it suggests that BNPL encourages consumers to overspend. Recent research in the Journal of Marketing also indicates that BNPL leads to consumers purchasing more frequently and in larger amounts - another clear advantage for retailers.

BNPL companies often market themselves as free, consumer-friendly alternatives to credit cards. In practice, how do these business models make money?

MG: BNPL providers make money on the interchange fees, similar to how credit card providers make money. Interestingly, the dollar amount that a BNPL provider puts into their pocket is higher than the interchange fees charged to retailers by credit card companies. I suspect this is where most of the revenue is coming from.

There is a potential downside for consumers in that retailers may ultimately pass interchange costs on to them through higher prices. This is an indirect and often unnoticed revenue driver for savvy retailers, especially compared to more visible sources like late fees.

Is there evidence that integrating BNPL into the checkout flow elevates purchase amounts?

MG: from leading marketing journals shows that BNPL increases spending. Ironically, increased consumer spending is an attractive selling point for retailers that adopt BNPL, while it is a red flag for consumer advocates and policymakers.

From a consumer psychology perspective, what makes BNPL so tempting?

MG: The research is telling when it comes to BNPL and temptation. Seeing a price displayed as a smaller installment amount compared to the full price of a product or service can feel a lot better and provide just the right amount of lubrication to move a consumer not only to buy, but also to increase spending on other items as well.

Consider a situation where you are on a major home outfitter’s website buying a cover for a bean bag chair. Its full price would cost you $132, or you could pay $12 per month with the BNPL option. The latter installment price could seem very attractive and may motivate you to add more items into your checkout cart, because after all... $12 doesn’t seem like very much.

Consumers often view BNPL as a softer, safer form of debt. In your view, is that a misconception with potential downsides, or can BNPL be part of healthy financial behaviour?

MG: For some people, BNPL could work perfectly fine. Data from the Financial Consumer Agency of Canada suggests it can help with budgeting or "bridging a timing gap" between purchases. That said, the findings warrant caution: the sample was small, only a third of respondents were familiar with BNPL, and the data offers little insight into how financially vulnerable Canadians use these products. The data also dates back to 2021; more recent evidence paints a darker picture:

- 42 per cent of adults have BNPL payments attached to their credit card (and not their bank account)

- 45 per cent of Canadians are carrying some kind of balance on their credit card

What do these stats add up to? Consumers are effectively paying interest on interest for purchases that may - or may not be - essential.

On top of this, data from a 2023 report by the U.S. Federal Reserve shows that BNPL users are already more likely to be financially stretched - with 78 per cent indicating that BNPL was the only way they could make a purchase.

The takeaway is unsettling: For many users, BNPL is not about convenience but about coping with financial constraints. When purchases depend on deferred payments, it signals deeper issues that cannot be solved by normalizing BNPL as a gentler form of debt.

If you could give online shoppers advice for staying financially healthy while using BNPL, what would it be?

MG: Don’t do it! I just can’t get behind BNPL when you consider the research. If you need to use any type of credit product - and let’s be real, that’s almost everyone - it’s critical to understand the impact on your budget and, where possible, pay off balances in full each month.